Daily Cashier Report Applet

Purpose and Overview

The Daily Cashier Report Applet is a simple and focused tool for checking your daily sales numbers. It helps you see exactly how much money was collected during the day and provides your final Z-Report (end-of-day summary).

While these reports are also available inside the main POS system, this applet gives you a dedicated space to review your financials without the distraction of the active selling screen.

Video Tutorial

For a visual walkthrough of the Daily Cashier Reports, watch the video below:

Why is this a separate applet?

We created a standalone applet for these reports to make your work easier:

- Focused Access: Managers and back-office staff can check sales totals and print reports without opening the full POS interface.

- Convenience: It allows you to review performance from any device, keeping the main POS counters free for serving customers.

- Clear Reconciliation: It provides a clean workspace specifically for matching your physical cash and card slips against the system’s records.

Key Features

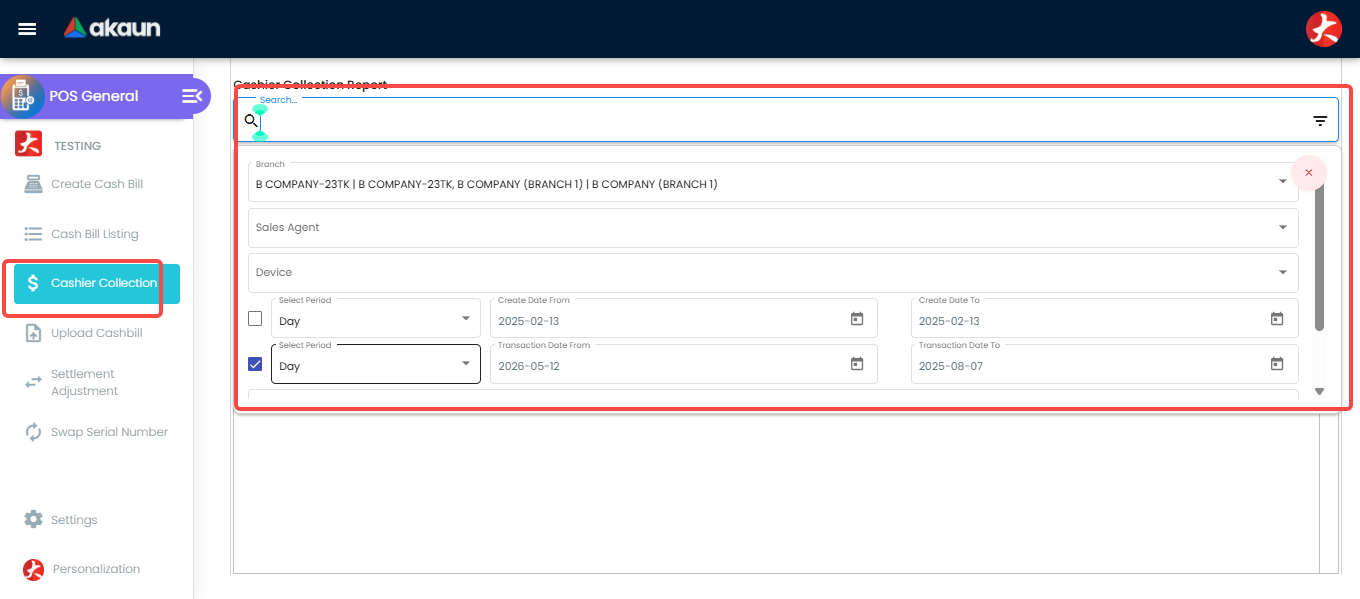

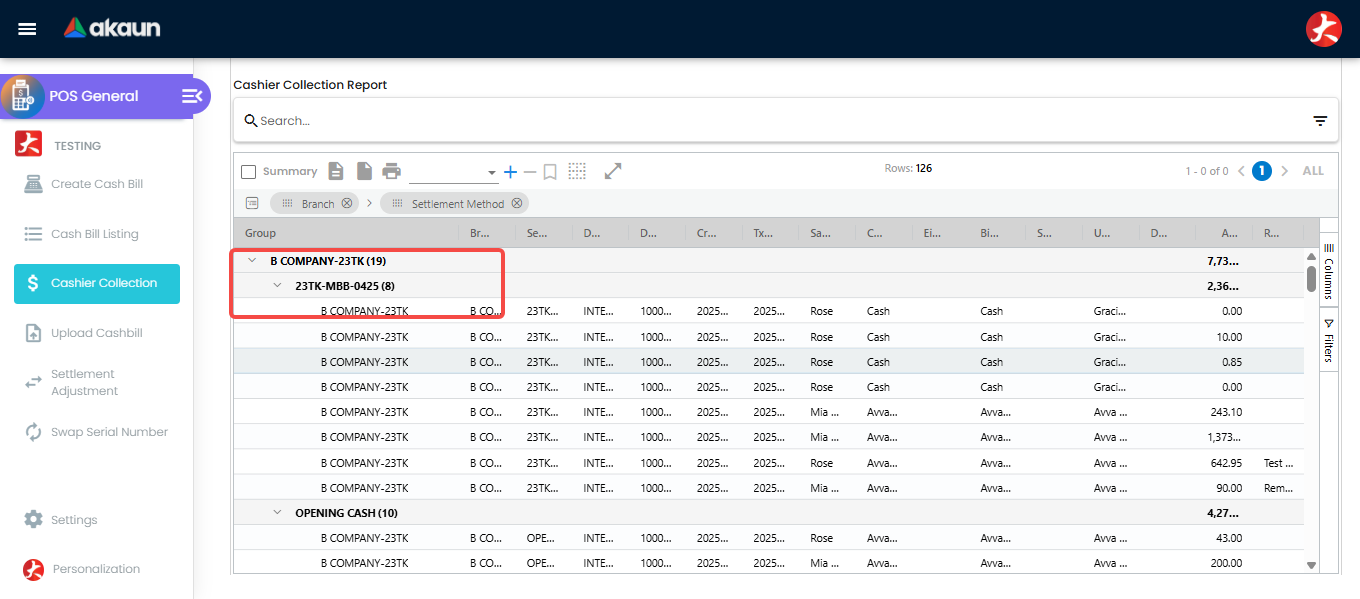

1. Cashier Collection Report

This tool shows you a list of all payments received. It is the best way to see how much money was collected by each payment method (like Cash, Credit Card, or E-Wallet).

How to use it:

Open the Cashier Collection menu.

Use the Advanced Search to select the date or store you want to review.

Use advanced search to filter your collection data. The report groups your totals by payment type. This makes it easy to count your physical cash and card slips and match them to the system.

Totals are organized by payment method for easy reconciliation.

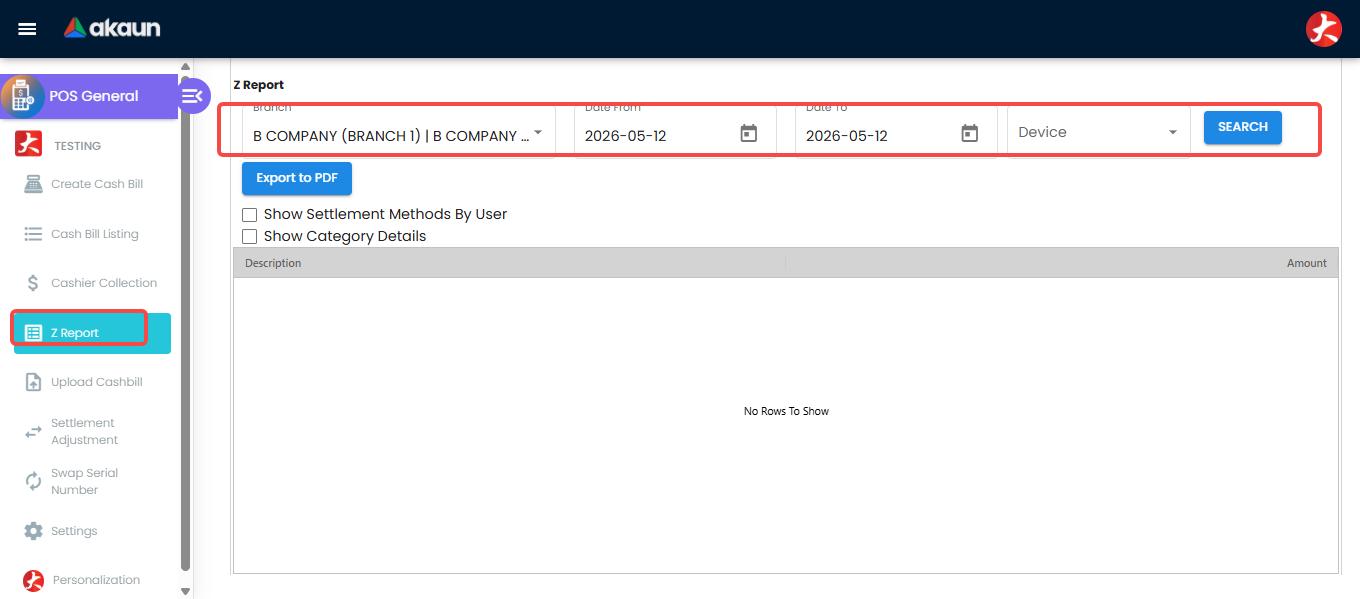

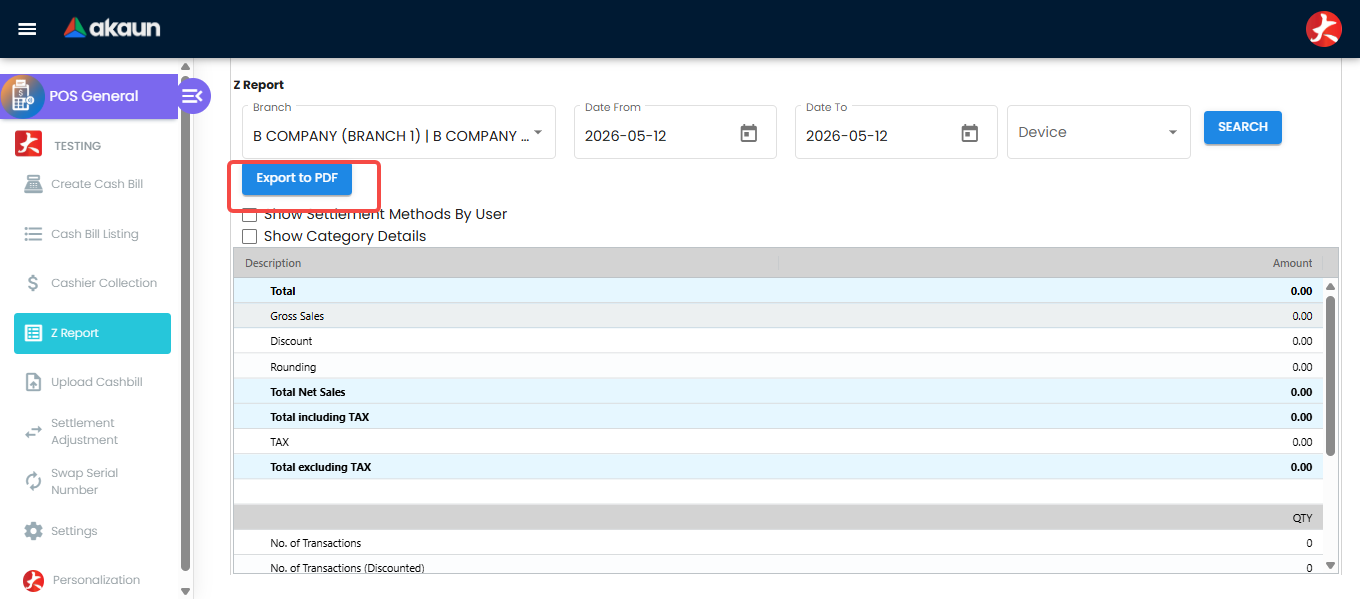

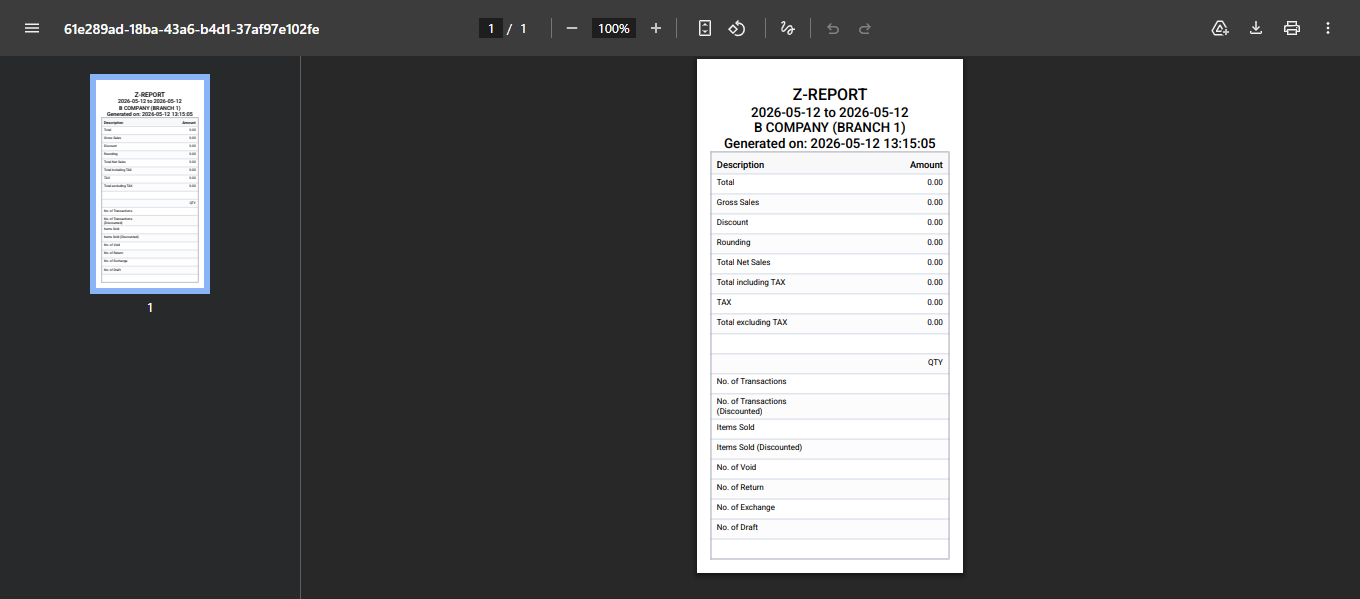

2. Daily Sales Summary (Z-Report)

The Z-Report is your final end-of-day summary. It shows your total sales, any canceled orders, and the final breakdown of all money collected.

How to get your Z-Report:

Select the relevant details (like Date and Store) to search for your report.

Find your daily sales summary report. You can save or print your report by clicking the Export to PDF button.

Click 'Export to PDF' to generate the document. Once the PDF is generated, you can print it for your physical records or send it to your finance team.

Print your final Z-Report for store closing.

Simple Daily Workflow

- Check Collections: Throughout the day or at the end of a shift, use the Cashier Collection tool to see how much money you should have in your drawer.

- Match the Numbers: Count your physical cash and card receipts. They should match the totals shown in the “Collection” report.

- Generate Z-Report: At the end of the day, use the Z-Report tool to create your final summary.

- Print and Close: Export the Z-Report to PDF and print it to finish your daily store operations.

Related Guides

- POS General Applet - The main tool for making sales

- Accounting Vaults - Where your sales data is automatically recorded